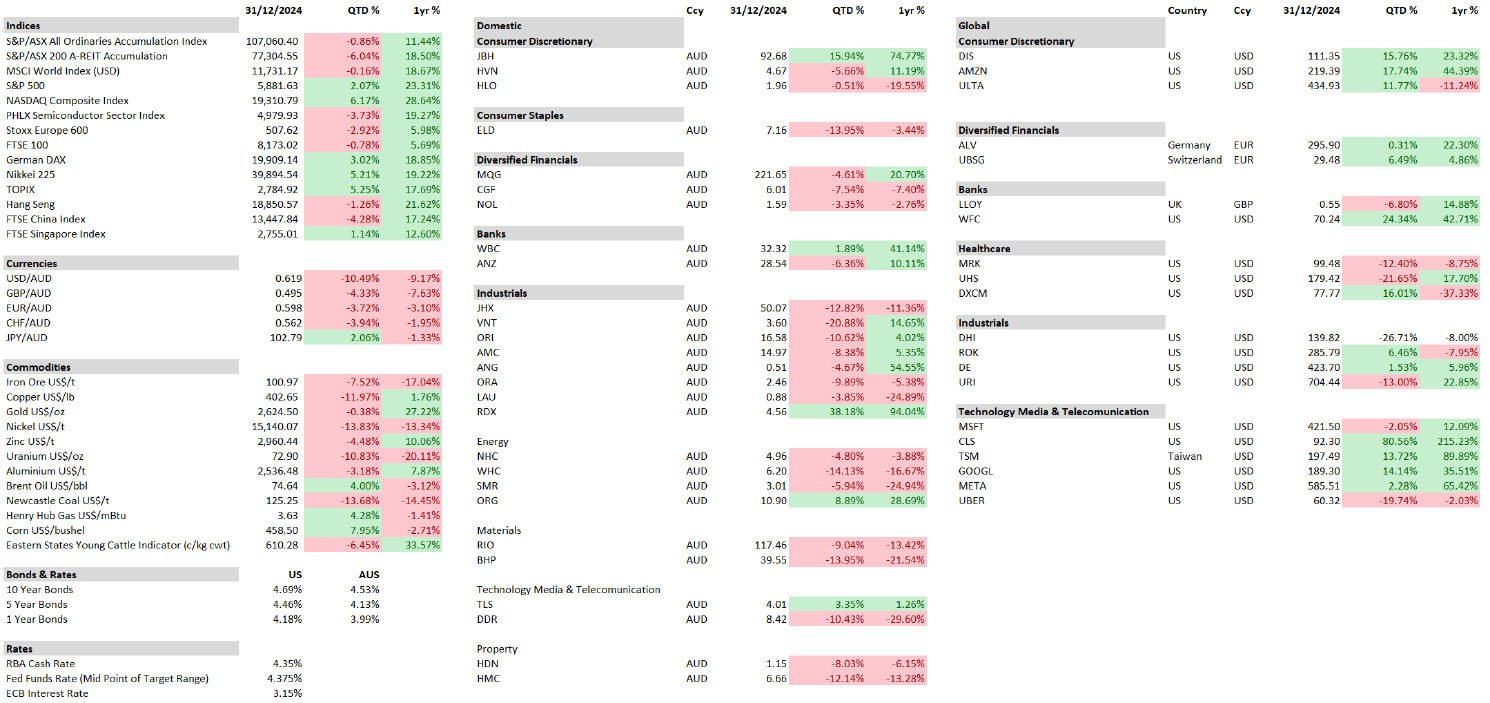

As at December 2024

Equity Market Returns

Source: Capital IQ, MSCI

Overview – Hugh MacNally

After two years in which Equities markets have risen strongly, concerns seem to be building that markets have become very stretched and that valuations are excessive. Our view is that the valuations are far from uniformly high and that there are a range of attractive opportunities to invest at high returns on capital.

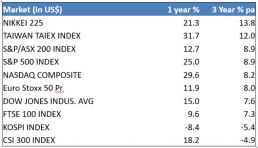

In the last 12 months global markets, as measured by the MSCI (a global stock index) finished the year up 30.78%. There has been a wide divergence of returns among individual markets, as is shown in the table below. The US markets rose strongly, particularly the NASDAQ, which is heavily weighted in tech stocks. The same was true of markets in Taiwan and Japan. The Chinese market (CSI 300), which had fallen over 50% in the preceding 3 ½ years was up 18.2%, recovering some of the lost ground. However, many markets did not rise anywhere nearly as strongly, particularly in Australian, UK and European markets (Euro Stoxx 50), which were up between 9.6% and 12.7%.

While the last twelve months have certainly produced very high returns for a number of industry sectors and particularly for major technology stocks, the returns over a longer period, say the last 3 years (right hand column below), have not been high at all. Apart from the Nikkei and the Taiwanese indices, the highest returns were from the Australian market and the US S&P500 and these were by no means exceptional at 8.9% p.a. Returns from European markets have been low, and understandably the Chinese markets suffering severe economic and property woes have been negative.

Source: Bloomberg - Returns in Local currencies.

Although much commentary has pointed to the rise of the tech sector, the broader picture does not indicate a runaway speculative market. Although, we are somewhat cautious of some of the tech sector prices, particularly among the AI favourites, most notably stocks such as Nvidia. Many of the mega tech companies while the prices are elevated, they are not excessive.

Unlike earlier bubbles, particularly in 2000, these companies have very healthy cash flow yields which are similar to bond yields and additionally, the cash flows are rising strongly. This gives us some comfort that the prices of equities are not generally excessive. One characteristic which is particularly evident among US stocks is a very high return on capital, which is an immense long-term positive.

As a long-term investment strategy, PPM looks at the prospects of individual companies rather than trying to predict the direction of markets; there are too many conflicting variables and market timing, which has to be spot on, is unreliable.

Turning to interest rates, short-term yields in most developed economies are falling as inflationary

pressures subside. In the US, the Federal Reserve has reduced the cash rate by 1%, in the UK rates have been reduced by 0.5%, Europe 1.35%, however, in Australia rates have to date been held steady by the Reserve Bank. Currently, short-term rates in Australia and the US are very similar, at 4.35% and 4.5% respectively.

While short-term rates and inflation have declined, central bankers have recently become somewhat cautious about declaring victory over inflation, perhaps remembering their unfortunate experience 50 years ago when they declared victory too early, with disastrous results.

As a result, and in contrast to short-term rates, longer-term bond yields have risen over the last twelve months. In the US by 0.75%, UK 1.10%, Europe in a range up to 0.65%. In Australia, the 10-year bond yield has risen 0.40% this year. The current bond yields we think are consistent with central banks achieving their target inflation rate of 2-3% and may not fall much from the current level. At 4-5%, they provide investors with a 2-3% real return, which is adequate, given the funding task that developed economy governments are faced with. A return to ultra-low yields would not seem likely and it would certainly not be attractive to the rational investor. Please see chart of short-term rates and bond yields later in this report.

The last 3 months have seen a significant appreciation in the US$ against major currencies. The appreciation has been most marked against the A$, which fell approximately 10% from 69c at the end of September to 62c at year’s end. This has resulted in a significant benefit to the portfolios with offshore exposures (which are heavily weighted to US stocks).

This does, however, leave the A$ at the bottom end of the range that it has typically traded in over the last 30-40 years. While greater confidence in the superiority of investment prospects priced in US$ would be required, this requirement we feel is not difficult to satisfy.

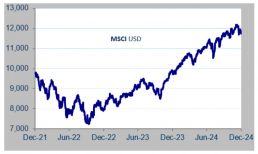

International Equities

Hugh MacNally

International Equities Performance

Source: MSCI

As outlined in the overview there was considerable variation in the performance of markets and industries over the last twelve months. Global equities markets in aggregate rose strongly for the quarter and the year. The MSCI, an index of global stocks, was up 30.78% for the year and 11.87% for the last quarter.

There continue to be attractive opportunities, particularly in the US market and during the quarter we added three companies to portfolios: Celestica Inc, Dexcom Inc and Uber.

Celestica offers solutions globally in advanced electronics, precision manufacturing, and complex systems integration. While the company operates in numerous industries, the strongest growth has been in data centres. Revenue growth has averaged over 13%p.a. over the last four years, and margins have improved post the company’s spinoff from IBM. The company is capitalised at US$11 billion and has a revenue of approximately US$10 billion. Returns on capital are extremely attractive, and we think that the growth will continue for an extended period of time, based on the growth plans of its blue-chip client base.

Dexcom Inc is a medical device technology company and leader in continuous glucose monitoring (CGM) systems for diabetes management. The devices provide real-time glucose data, enabling patients and healthcare providers to optimize treatment and improve outcomes. The company operates worldwide, but the US market is the dominant source of revenue and profit. Dexcom is capitalised at US$30 billion and currently has revenue of approximately US$4 billion. Growth opportunities are substantial, and the device is critical in the treatment of Type 1 diabetes in particular. Margins and returns on capital are very attractive.

Uber is, of course, the well-known global ride hailing service. What is probably less well known is the financial success that the company has achieved in the last two years. In common with many tech companies, Uber has had strong revenue growth and very high rates of return on capital. In the key markets in which it operates, it is mostly the dominant player and the brand that everyone knows. As is also the case in these types of industries, profitability is heavily skewed in favour of the dominant player. Operating cashflow has increased rapidly, however this has only required low levels of capital investment, resulting in a substantial increase in free cash flow. There seems to be no indication of slowing in these numbers, and improvements in key metrics have been consistent.

The Uber share price is about the same as it was 12 months ago as some market concern has arisen over the role of automated taxis. Our view is the concern is misplaced, and that Uber will continue to be one of the key parts of a changing transport ecosystem. Automation technology, when it becomes widespread, which optimistically will take some considerable time, is another part which may expand the size of the market. Currently, Uber has revenue of US$44 billion, up 30%p.a. over the last 3 years.

During the year, we quit a long-held position in the major pharmaceutical company Merck, the developer of blockbuster oncology drug Keytruda. While we made a reasonable return on the earliest purchases (11.4% p.a.) the return did not reflect the magnitude of the success the company had in the laboratory. Our view is that the return on investment in the pharmaceutical industry is not high enough to be attractive. High cost of research and the short life of patents combine to stack the odds against the investor. It may come as a surprise, as drug prices are seen as immorally high, that the return on capital for pharmaceutical companies is actually not high. As an indication of the problem, over the last 25 years the return of the S&P Pharma Index has only been marginally above the return on cash – not the sort of odds we really like.

We are also in the process of selling the holding in Moderna, which has been very disappointing and while we are reluctant to sell at the current price, we think that what has been true of Merck will also be true of Moderna.

Rockwell Automation, Inc. is a global leader in industrial automation. The company provides advanced hardware, software, and services to optimize manufacturing and production processes for the automotive, energy, and life sciences industries. The sales and earnings growth have been disappointing and while the company operates in an attractive industry the hoped for operating returns have not materialised. There seem to be more attractive opportunities, and this position is being progressively sold.

We have topped up the holdings in Alphabet, which had lagged the market for much of this financial year as attention shifted to higher profile AI stocks. Ironically, Google has long been one of the leading lights in AI. There have been a number of regulatory concerns that have arisen over the recent past, but we feel that the attractiveness of Alphabet’s businesses outweighs these concerns.

Falls in the share prices of a few of our favourite non-tech companies have also presented opportunities to top up holdings. Two of note are: DR Horton, the largest residential builder in the US and United Rentals, the largest plant hire business in the US. After very strong rises, on exceptional operating results, these companies have retraced some of the gains we think this provides an opportunity to acquire stock at an attractive price.

Additionally, two very successful companies, which have been under pressure, for reasons related to short-term industry conditions, started to recover during the last quarter. We are optimistic that the remedial actions they have taken during these difficult times will benefit their longer-term future.

In the agriculture sector, equipment manufacturer, Deere and Co. suffered a significant downturn in demand largely influenced by cyclical factors in the industry. In a completely different industry, Ulta Beauty, the largest retailer of cosmetics and beauty products in the US (similar to Mecca in the domestic market) started to recover after declining 40% over the last year. Both these stocks are attractively priced after the decline in prices.

It might be noted that there is a very high weighting in US based companies. This has not been by design, but has resulted from a focus on operating results, which US companies have generated superior results. It should also be noted that many of these companies are global in their operations and have been among the most successful in developing markets outside their home market. We have not excluded other developed markets, but struggle to find better candidates at better prices.

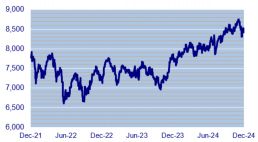

Australian Equities

Peter Reed

Australian Equities Performance

Source: Bloomberg

Australian equities delivered -0.86% return for the quarter ended December 2024 and +11.44% for the calendar year.

A new position was established in Austin Engineering. Although the company is relatively small size – market cap $335mil, we believe it is sufficiently high quality to warrant inclusion in the domestic core equity portfolio.

With over 50 years of experience, Austin collaborates with leading miners and original equipment manufacturers (OEMs) to deliver customised engineering solutions for mining operations. The product portfolio consists of dump truck trays, buckets and ancillary products, complemented by repair and maintenance services.

The company’s competitive strength lies in its focus on innovation, deep industry expertise, and its extensive global footprint. Austin operates across key markets in Australasia, North America, and South America, with plans to expand into additional regions, further strengthening its international presence.

The business maintains lower capital intensity relative to industry benchmarks, reflecting efficient asset utilisation and a higher turnover rate. This leads to decreased fixed costs as a percentage of revenue and improved returns on capital employed.

Recent financial performance underscores the company’s strong growth trajectory. Since implementing a strategic reset in 2021, Austin has achieved a 75% increase in revenue, a 50% improvement in margins, and a more than twofold increase in returns. The outlook remains highly positive, with a current order book valued at A$190 million, growing at an annual compound rate of 44%.

Dexus, a significant player in the Australian property market, was added to the portfolios during the quarter. We exited our last property holding back in mid-2023 with the sale of HDN – HomeCo Daily Needs Reit, on valuation grounds. It’s interesting to note that HDN’s share price has remained largely unchanged since that point and is reflective of the broader property sector. As such we have been content to remain on the sidelines, waiting for more attractive investment opportunities to present themselves.

One such opportunity, we believe, comes in an out-of-favour portion of the property market: offices, the main focus of Dexus. The sector overall has been afflicted with high vacancy levels as the fallout from covid impacted work habits and the work-from-home phenomenon took hold.

This situation will normalise over time but what is interesting to see is a bifurcation of the market, with the premium end well supported as businesses upgrade to higher quality space. Visibility of supply is good for big ticket offices and we expect this to remain constrained for at least 4 to 5 years. This all implies positive rental dynamics for landlords.

As the upgrading process works its way through and businesses vacate lower grade office space the quality divide will play to the benefit of Dexus with its focus on premium space in prime CBD locations. We cover Dexus in more detail in the property section of this report.

Packaging giant Amcor announced, in an all-stock deal, they would merge with US-listed Berry Group, creating one of the largest packaging groups in the world with annual revenue of $24billion.

Although Amcor has a history of making small-scale bolt on acquisitions, the size of this transaction – Berry is only 15% smaller than Amcor on a profit basis – stands out. Recognising heightened risks associated with large acquisitions, our position at this stage with the merged entity is to hold and observe progress around merger targets. These include synergy benefits of $650mil pa (starting year-3) as well as a lift in revenue growth above market by 1% while delivering improved profit margins.

Ventia, our industrial services company, faced ACCC allegations of collusion in bidding for defence-related contracts. Although it is early days in this case and only limited information has been released, we observe that Ventia’s defence work is normally low margin work, not a typical area for profit padding. We would also observe that the ACCC does not have an uncheckered record when alleging breaches of consumer protection laws. Given already attractive valuations for the stock, our instinct is to use the share price pullback as an opportunity to add further to our position.

At this point, with solid gains in the index having been registered over the past 12 months, it is worth taking stock of where the overall market is sitting from a valuation perspective.

Source: Bloomberg

The chart indicates that stock gains have taken broad market valuations (market price earnings ratio) toward the top of the decade’s range (excluding the covid period). We would observe that while we continue to find attractively priced opportunities (Ventia, Dexus as examples) there are other sections of the market where valuation is problematic. Most notable, given their size in the market, are banks and financials, as well as technology. Our portfolio positioning continues to hold low exposure to these areas.

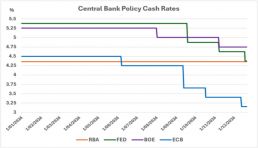

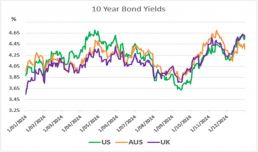

Interest Rates

Neil Sahai

90 Day Bank Bill (%) vs 10 Year Bond (%) Performance

Source: Bloomberg

After much anticipation, central banks worldwide have commenced or continued easing policy rates this quarter. The Bank of England (BOE) reduced rates by 25 basis points to 4.75% in November. The Federal Reserve (FED) executed two 25 basis point rate cuts, one in October and another in December. Meanwhile, the European Central Bank (ECB) decreased rates by 25 basis points in October and another 25 basis points in December, bringing rates to 3.15%. The chart below illustrates the latest actions by the BOE, FED, and ECB.

Source: Bloomberg

December proved to be a pivotal month for monetary policymakers, as their recent commentary indicated that inflation is moving in the right direction and interest rate cuts are achieving their intended effect. However, they emphasized a cautious approach moving forward, given the heightened economic uncertainty.

Source: Bloomberg

Despite the fall in cash interest rates (excluding Australia), bond yields in developed economies have been trending upwards. This divergence of these two trends has brought the yield curve closer to normal; interpretations of the significance of this are difficult to be definitive about at this time.

Expectations for U.S. interest rate cuts in 2025 were significantly scaled back following the forward guidance provided by Federal Reserve Chairman Powell during the December meeting, indicating a more conservative view of future declines in inflation. Additionally, concerns over the effects of potential trade policies have come into play post the US election.

This shift in market outlook, coupled with weakness in commodity markets, has negatively impacted the Australian dollar, which has dropped to a two-year low of 62 cents against the U.S. dollar.

Finally, the Reserve Bank of Australia (RBA) has left rates unchanged, although it should be observed, that they did not raise rates as far as occurred elsewhere. The minutes of the December meeting suggested that the chance of a rate cut is improving. However, the inflationary effect of a weaker dollar adds an extra layer of complexity, as does the proximity of a federal election.

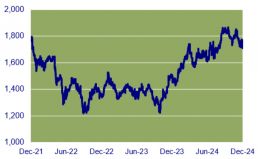

Property (REITS)

Franklin Djohan

ASX Property Graph

Source: Bloomberg

The property index gave back some of its gains during 2024, ending the quarter down 6.04%. However, the A-REITs still posted a strong performance for the calendar year, gaining 12.07%, significantly outperforming the broader All Ordinaries Index.

As noted in the previous quarter, the appeal of the listed property sector is becoming more evident. While some well-known names have seen significant share price gains, certain sub-sectors continue to offer compelling valuations, particularly the office sector.

Investor sentiment towards Australia’s $350 billion office tower market is beginning to shift, with a rise in transaction activity and signs that valuations—down by as much as 20-30% from their peak—are stabilising. This recovery is nuanced, influenced by factors such as location, precinct, building quality, and income structure. Challenges persist in the broader office sector, particularly with subdued private sector rental demand. However, specific precincts like Sydney’s core CBD are experiencing increased demand amidst constrained supply. Additionally, newer offices with higher sustainability ratings are in high demand, contributing to rising net effective rents across premium office spaces.

Dexus is a listed Australian real estate investment trust (A-REIT) that specialises in owning, managing, and developing office and industrial properties. The company has built a strong reputation as one of Australia’s premier property groups, managing a high-quality portfolio across key metropolitan markets. The company also operates an extensive funds management platform, managing properties on behalf of institutional and retail investors. This platform allows Dexus to diversify its income streams and build strategic partnerships.

However, despite its broader ambitions to become a fund manager, Dexus still stands out as a prime way to invest in the office recovery.

Dexus has significantly repositioned its office portfolio in recent years, with 96% of its offices now located in prime locations and 55% classified as premium grade. During the quarter, Dexus sold two offices: 100-130 Harris Street, Pyrmont, for $229.3 million, and 145 Ann Street, Brisbane, for $213.9 million. These transactions are part of a broader strategy to divest approximately $2 billion worth of assets over the next three years. This initiative aligns with Dexus’s ongoing efforts to consolidate its office portfolio within the central core of Sydney’s CBD while also strengthening its balance sheet.

This strategic shift has enabled Dexus to outperform the broader market, achieving higher occupancy rates and attracting lower incentives.

Despite its strong weighting in the Sydney core and improving operational performance, Dexus continues to trade at a substantial discount to its Net Tangible Assets (NTA), presenting an appealing investment opportunity.

PPM is continuously looking for ways to improve the service we provide to you and your feedback is important to us. We hope are staying safe and healthy. Please contact Jill May, Head of Client Relationships with any questions, comments or suggested improvements at jm@ppmfunds.com or on (02) 8256 3712.

Private Portfolio Managers Pty Limited ACN 069 865 827, AFSL 241058 (PPM). The information provided in this document is intended for general use only and is taken from sources which are believed to be accurate. PPM accepts no liability of any kind to any person who relies on the information contained in this document. The information presented, and products and services described in this document do not take into account any individuals objectives, financial situation or needs. The information provided does not constitute investment advice. You should assess whether the information is appropriate for you and consider talking to a financial adviser before making any investment decision. Past performance is not necessarily indicative of future returns. © Copyright Private Portfolio Managers Pty Limited ABN 50 069 865 827, AFS Licence No. 241058.

Your Investment Management Team

Hugh MacNally

Portfolio Manager,

Executive Chairman

Peter Reed

Portfolio Manager,

Director

Franklin Djohan

Portfolio Manager / Analyst

Max Herron-Vellacott

Portfolio Manager

Neil Sahai

Portfolio Manager