As at September 2024

Equity Market Returns

Source: Capital IQ, MSCI

Overview – Hugh MacNally

Equities markets rose significantly over the last 12 months and the last quarter.

The Australian dollar appreciated against a range of currencies. Against the US Dollar the A$ was up 9%, the strength was most pronounced in the last six months as it became apparent that the US would reduce interest rates well before Australia.

While cash rates were unchanged in Australia, short-term bond yields have fallen from 4.5% to 3.5% over the last 12 months. Interestingly, given the declines across the yield curve, residential mortgage rates are only marginally down on the highs of July to be currently just below 6%. This compares to the fall in cost of US mortgages of over 1.5%. The mortgage holder demographic in Australia is yet to benefit in the way their US counterpart has.

Of major significance to the Australian market and economy the iron ore price has been in steady decline for the last 9 months and is 25% below that of 12 months ago. The weakness in the demand from China (the dominant customer) has been widely discussed. Despite China’s recent economic stimulus, the extraordinarily favourable conditions that have existed for 20 years seem to be becoming less favourable. Maturing demand and rising supply will test BHP and RIO’s pricing discipline. Copper on the other hand has risen 27% this year, although the value of the market is small compared to the bulk commodities.

Of importance to the investment in agricultural services and equipment, there was a large decline in grain prices this year. Soya beans and corn fell 19% and 15% respectively. This puts them back to the lows of the last 20 years and we think this is a favourable time to invest.

Despite negative reporting on economic conditions, results from the recent company reporting season, both domestically and globally, have been encouraging. As is discussed below in more detail many industries have weathered the higher interest rate environment well. With interest rates falling widely, relief is being experienced by consumers.

While the pricing of stocks in the tech sector is high it is not that of previous tech bubbles, except in a small number of companies, such as the fabled Nvidia. In many other industries we think there are attractive situations.

International Equities

Hugh MacNally

International Equities Performance

Source: MSCI

For the last 12 months global markets were up 23.2% and 2.4% for the last quarter as measured by the MSCI, a global index of stocks in A$.

Looking at the main stocks held in the portfolios, sales and earnings growth for the last 12 months and for the last quarter varied significantly between industries as can be seen from the table below.

Source: Bloomberg

The most important observations we would make are:

Growth in sales and earnings in the technology sector were extremely high. Amazon, Meta Platforms (previously known as Facebook) Taiwan Semiconductor and Alphabet (Google) all had extraordinarily strong growth in profit over both periods. Microsoft less so, but earnings growth was still close to 10% for the year. This performance was common in major companies in the sector. As we have commented during the year, valuations are high, but not excessive among the portfolio stocks. There are, however, numerous companies where valuations are excessive and over the last 12 months, we have sold holdings for example in Nvidia and Intuitive Surgical. Both great companies with very good opportunities, but the valuations reflected those of a bubble (which we do not think is the case generally).

Elsewhere, results were more mixed, however, were better in the last quarter than for the year. This supported our view that operating conditions in a wide range were improving as companies adjusted to higher interest rates. Valuations in these industries are quite attractive and we feel there are opportunities to acquire high quality companies. United rentals is a good example we have previously mentioned, where we think the increased growth in the last quarter is significant. Similarly, Universal Health, a large hospital operator, recovered from the disruptions caused by Covid, which included very high increases in labour costs.

We hold a number of very high-quality companies, which were bought on a counter cyclic basis. They have been affected by short-term issues which are reflected in recent sales and profit numbers. Their share prices fell sharply over the last two years and valuations are now extremely attractive in our view. The companies are: Ulta Beauty, Deere and Co. and Rockwell Automation. Deere and Co., for instance, is merely suffering from an adverse stage in the agriculture cycle. The company is one of the leaders in the field and has a long history of produced high returns.

The finance sector (Wells Fargo, UBS and Allianz) had a reasonably good year operationally and a better last quarter. We have not included comparative figures for UBS, as its extraordinary acquisition of Credit Swiss made prior period numbers incompatible. We generally don’t like large acquisitions as they are almost always made at high prices, however, in this case we have no complaints (if only other acquisitions could be made at such a discount!). Wells Fargo returns are gradually improving and their regulatory issues (which have weighed on them for seven years) are being resolved. They have had little deterioration in the quality of their lending books and have made a strategic shift which seems to be bearing fruit. Allianz has benefitted from a good insurance environment.

During the quarter we sold a long-held position in Merck Inc, a pharmaceutical company. We have been a little disappointed in the return we have had from the company and think it might be an industry wide problem. Merck developed Keytruda, one of the most successful drugs this century, which reached annual sales of over $25 billion over the last 10 years, yet the return for Merck has been barely above 10% p.a. over this period – having such success in the laboratory has not been reflected in investment return. This is perhaps because of the brief life of patents – Merck’s patent for Keytruda runs out in 2028 and while they may be able to extend it by various means, that is by no means certain. Patents are significantly less valuable in the pharmaceutical industry than in other technologies.

The biggest global weighting in the portfolios is to US companies. Not only is the return on capital for their big tech stocks extremely high, but in other industries it is also higher for comparable companies elsewhere. A full explanation of this would occupy a volume, but productivity growth, flexibility of labour and the size of their domestic market is important.

Australian Equities

Peter Reed

Australian Equities Performance

Source: Capital IQ

The Australian equity market rose in line with global markets during the quarter to register a total return of 7.85%. Leading sectors included: Industrials; Real estate; Consumer discretionary. Lagging sectors included: Energy; Utilities; Consumer staples.

The real estate sector has lagged the broader market significantly since the covid downturn. However, as business conditions normalise and as prospects for a change in direction of interest rates have emerged, we have, over the past several quarters, seen a lift in the sector.

Despite conditions in the office market remaining generally difficult, we are open to the quality end of this sub-sector, where demand is benefitting as tenants “trade up.” We are also of the view that valuations are close to a cyclical bottom, and which should see a boost from a normalisation of work routines between office and home. Work from home, of course, has been a headwind for the sector since covid. We will have more to say on this opportunity in future reporting.

The consumer discretionary sector has benefitted from similar factors to property, particularly regarding the interest rate outlook. Our two main positions here are JB HiFi and Harvey Norman. JBH has been the outstanding performer in this segment as its business model has proven most adaptable to volatile conditions – think of lockdowns where retailers’ online capabilities were crucial – while riding the wave of demand for consumer electronics and software.

For HVN, the journey has been more difficult as the business is more heavily leveraged to the housing cycle. This has been a headwind for some time now as the industry goes through one of its more severe downturns. Pleasingly, results announced by the company during the quarter indicate that this headwind is abating. For the 2024 financial year, HVN’s Australian franchise sales declined 6% but, of note, second half sales performance saw a marked improvement to be down only 1%. If we extend our view further, we see July sales (which fall in FY25) registered growth of 3.3%. Further, commentary from company management takes a positive view on demand implications of artificial intelligence (AI), as it becomes embedded in the personal computer (PC) market.

A new position was established during the quarter in Ventia, a leading service and maintenance provider in Australia and New Zealand, focusing on key segments like Defence & Social Infrastructure, Infrastructure Services, Telecommunications, and Transport. The company consistently delivers high returns, improved margins, and strong cash conversion, distributing 60-80% of its profits to shareholders.

A significant achievement of Ventia’s management is the strategic shift away from riskier design and construction projects towards service and maintenance contracts. This move has led to diversified revenue streams across various industries and markets, serving a broad customer base composed of two-thirds governments and government agencies and one-third large private enterprises.

The company’s contracts are a balanced mix of long and short durations, averaging seven years, with about 80% of contracts indexed or having annual price resets, reducing the typical pricing risks associated with such industries. Ventia’s disciplined operations and defensive approach make it a stable investment choice with significant growth potential. Management estimates the company’s market share at 10%, and with a growing asset base, increasing outsourcing trends, energy transition, and digitalisation, Ventia is strategically positioned for future growth.

The utilities sector came in for a bout of profit taking during the quarter following a strong run. As mentioned in the previous quarter’s commentary, we established an initial position in Origin toward the end of last quarter and added to the position throughout this quarter. The structural tailwinds bode well for the sector over the medium to long term and therefore we would expect any share price pullback to be temporary. At current price levels around $10, we view the stock as attractively priced, capable of delivering a rate of return comfortably above our 10% pa return benchmark.

Consumer staples has been another market laggard. PPM, until early 2024, held a position in Woolworths, exiting the stock on valuation grounds. The dominance of the two major players, Woolworths and Coles, has allowed us to take advantage of bad news as it relates to either of these stocks on the view that they will eventually remediate their position. This may take time and sometimes involve a change of management, but pressure eventually builds to deliver the necessary changes. It has also been an observation that among the major players, when Woolworths is facing difficulties, Coles is doing well, and vice versa.

Since our sale of Woolworths, the company has had to deal with the cost of living “crisis” and allegations that the supermarkets are price gouging. Negative sentiment will likely persist for a while along with the threat of ACCC intervention. During this period, we will be focused on two aspects: the prospect of corporate restructuring with potential to improve returns; and valuation returning to attractive levels. The still-attractive industry structure, despite the ever-present competition provided by the likes of Aldi and Costco, means that we retain our interest in possible reinvestment in the sector.

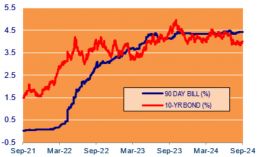

Interest Rates

Neil Sahai

90 Day Bank Bill (%) vs 10 Year Bond (%) Performance

Source: Capital IQ

After some false starts and hesitations, the interest rate cycle worldwide appears to be turning positive as inflation expectations ease.

The US Federal Open Market Committee (FOMC) lowered the Federal Funds rate by ½ percentage point to 4-3/4 to 5 percent at its September meeting as the Committee “gained confidence that inflation is moving sustainably toward 2 percent and judges that the risks to achieving its employment and inflation goals are roughly in balance.” The Fed’s dot point projections point to two more 25bp cuts this year.

The day after the FOMC meeting the Bank of England Monetary Policy Committee (MPC) maintained the Bank Rate at 5%, having reduced the rate by .25 percentage points at its July meeting, as it awaits data confirming inflation has stabilised.

The European Central Bank (ECB) is expressing its confidence that inflation will fall to its 2% target and that this will be reflected in the next policy move. ECB President Christine Lagarde is quoted as saying “The latest developments strengthen our confidence that inflation will return to target in a timely manner.”

In Australia, the Reserve Bank (RBA) has left the cash rate unchanged at 4.35% as although inflation has fallen since the peak in 2022 it is still some way above the midpoint of the 2-3 percent target range. As the cash rate in Australia is well below rates in the US and UK, it is hard to envisage any rate cuts until this gap begins to close.

Property (REITS)

Franklin Djohan

ASX Property Graph

Source: Capital IQ

The A-REIT sector posted a very strong quarter, delivering an impressive 14.3% return. Encouragingly, the gains were broad-based across the constituents of the index. Charter Hall Group led the way with a remarkable 42.8% gain, while Goodman Group, despite a solid performance, posted a more modest 6.45%—one of the lower gains in the sector.

The backdrop for the property sector has turned more positive. Given the sector’s sensitivity to interest rates, the market appears to be pricing in a more benign interest rate stance from the Reserve Bank. The expectation is that the downward pressure on asset values is now nearing its end.

The financing environment for commercial property in Australia has also improved, thanks to materially lower swap rates, tighter margins on new debt, and an increased willingness of banks to lend. This is expected to support the reopening of the transactional market, which had been subdued since the start of interest rate hikes.

Operational metrics across most property sub-sectors have remained resilient, supporting healthy rental growth. Earnings growth for the property sector is anticipated to be around 5-6% over the next few years.

After a strong share price run, many property stocks are now trading near or even above their Net Asset Values (NAVs). However, some sub-sectors still offer compelling valuations, trading at a significant discount to NAVs. One of these is the office sector.

While the office market remains generally challenging, with incentives still high at around 35% and vacancy rates hovering in the mid-teens, we see potential in a specific segment. There is a clear bifurcation within the office market, driven by the ongoing trend of premiumisation. Vacancy rates in premium office spaces are much lower compared to the broader market, and incentives in this sub-sector have marginally decreased. Net effective rents for premium offices have gradually recovered, while the rest of the market remains flat.

Despite these improvements in the premium office segment, valuations for office REITs remain depressed, presenting a potentially attractive opportunity.

PPM is continuously looking for ways to improve the service we provide to you and your feedback is important to us. We hope are staying safe and healthy. Please contact Jill May, Head of Client Relationships with any questions, comments or suggested improvements at jm@ppmfunds.com or on (02) 8256 3712.

Private Portfolio Managers Pty Limited ACN 069 865 827, AFSL 241058 (PPM). The information provided in this document is intended for general use only and is taken from sources which are believed to be accurate. PPM accepts no liability of any kind to any person who relies on the information contained in this document. The information presented, and products and services described in this document do not take into account any individuals objectives, financial situation or needs. The information provided does not constitute investment advice. You should assess whether the information is appropriate for you and consider talking to a financial adviser before making any investment decision. Past performance is not necessarily indicative of future returns. © Copyright Private Portfolio Managers Pty Limited ABN 50 069 865 827, AFS Licence No. 241058.

Your Investment Management Team

Hugh MacNally

Portfolio Manager,

Executive Chairman

Peter Reed

Portfolio Manager,

Director

Franklin Djohan

Portfolio Manager / Analyst

Max Herron-Vellacott

Portfolio Manager

Neil Sahai

Portfolio Manager