As at March 2025

Equity Market Returns

Source: Capital IQ, MSCI

Overview – Hugh MacNally

The tariff decisions made by the Trump administration are some of the worst pieces of economic policy in living memory. From early readings of opinion within the US, the view seems to be that the tariffs are going to hurt the US as much as those on whom it is imposed. If views now emerging are to be believed there seems there is only very luke-warm support. Senior business leaders are coming out and pointing to the immense issues for US global companies, such as Apple and other tech stocks.

The 20 largest companies in the US (market capitalisation over $20 Trillion) have global operations, something they have been uniquely successful in building. In most industries, a US company is dominant, has the highest return on capital and the best management. What an enormous own goal to throw a spanner in this immensely successful achievement.

As was commented on by Greg Ip in the Wall Street Journal (WSJ), the fear is the US has abandoned the global trading system that it has built over the last 50 years. This would be illogical and harmful to the largest companies in the US.

It points to President Nixon having raised tariffs by 10% in the 1970s, with the object of having other countries revalue their currencies. Once that occurred (this was in the days of fixed currencies and the gold standard) the tariff was removed. One can only hope that the removal of non-tariff barriers is the objective of this administration, but it is not clear whether this is the case.

As is discussed below, global stocks, which had fallen 1.8% during the quarter, fell an additional 10% in the few days after the tariffs were announced. Falls among major markets were in a relatively narrow range around this level.

The Australian market was down 3.3% for the quarter and fell another 6% post 31 March. The market rose 2% over the last 12 months.

The property sector performance as measured by the A-REIT Index was down 6.8% for the quarter and 5.4% for the year. However, this was largely due to the performance of data-

centre property. In other sectors, the picture is more positive and stocks such as Mirvac performed well.

Interest rates were reduced by 0.25% during the quarter by developed economy central banks, with the exception of the European Central Bank, which reduced rates by 0.5% citing weaker economic conditions. A cautious attitude was adopted regarding further falls. Post the tariff imposition, the Fed re-iterated its view that the progress of the fight against inflation would drive further reductions.

Bond yields fell during the quarter, except in Germany and Japan, where they rose strongly. Post tariffs, yields dropped sharply with fears of recession and flight to safety outweighing concerns about inflationary effects of a tariff.

International Equities

Hugh MacNally

International Equities Performance

Source: MSCI

Global markets, as measured by the MSCI, a global index of stocks, fell 1.8% over the quarter, but rose 7.0% over the 12 months to 31 March 2025.

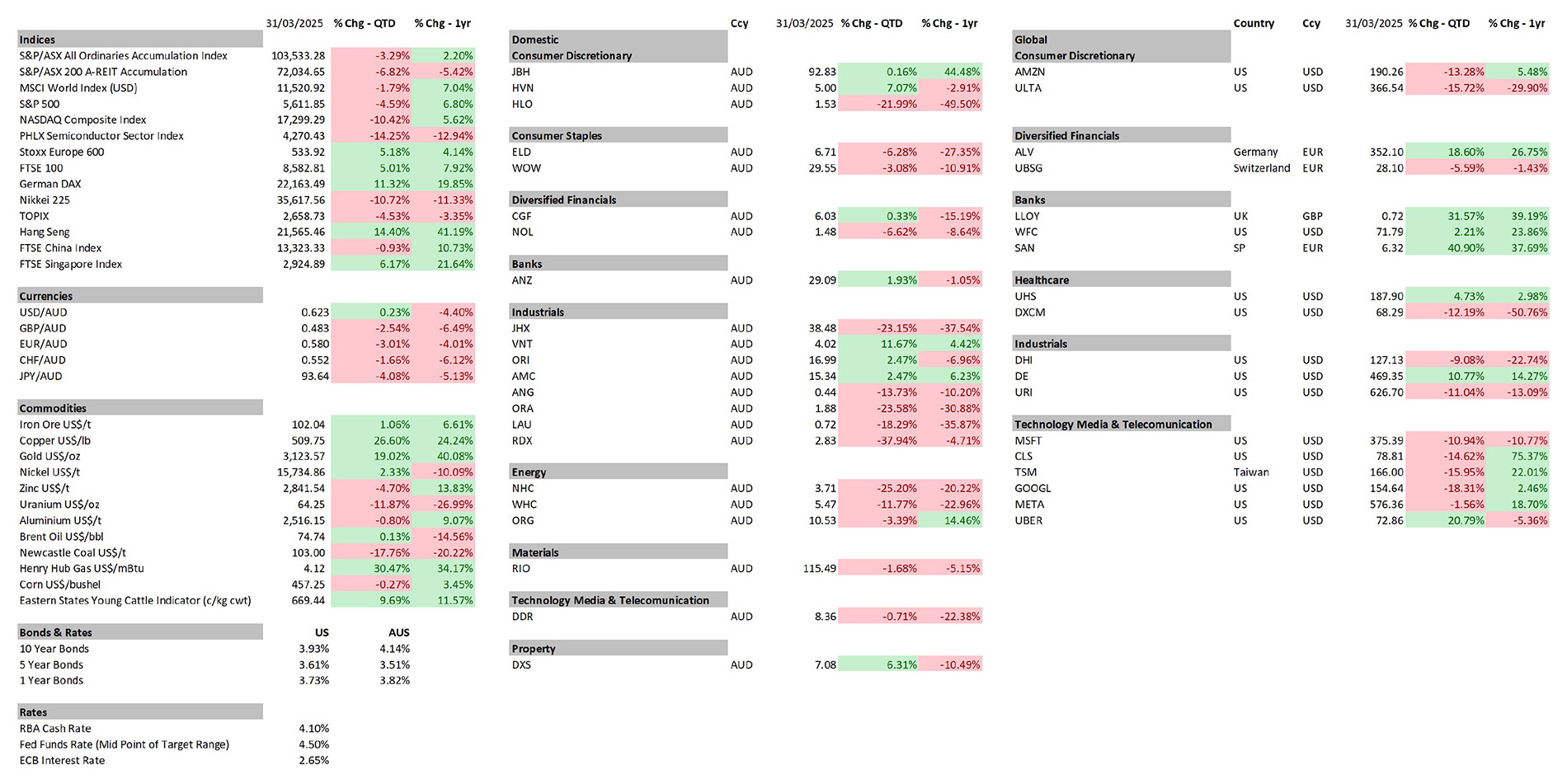

Post the end of the quarter markets fell heavily, as a result of the tariff announcements made by President Trump. The table below shows the declines in important indices to 7 April.

Source: Bloomberg

As can be seen, the falls over a few days were significant, but consistent across markets, and the decline in the US was pretty much the same as that for the countries on which the tariffs were being imposed. The MSCI was down 10%, as was the UK. The European market (Euro Stoxx 50) was down slightly more, as was the Japanese market. The Chinese markets varied with the Hong Kong index down 14.2% and the mainland market down 7.7%.

Among the portfolio stocks, banks declined the most, ranging from UBS (-16%) to Lloyds (-11%). Concern about loan deterioration and lower commercial activity was cited as a cause. Technology stocks declined between 12% and 4.5% for Alphabet. The core technology stocks Microsoft, Amazon, Meta, and Alphabet were less affected than the overall markets, although they had started to fall from mid-February. With the exception of Uber (up 8%) these stocks declined 15-20 % from the beginning of the calendar year.

It might be remembered that these stocks rose very strongly in 2024 and had become a little overpriced (again, with the exception of Uber). We retain our optimistic view of these stocks and expect earnings growth to continue. The results for these companies, which will be released within a month, are expected to support this view. This may represent an opportunity to build positions up to target levels for portfolios where there has not been much investment. New portfolios have not made much investment in this area in 2025 because we viewed the valuation as being not compellingly attractive (additionally, holdings were reduced where they had moved too far above target).

The main industrial stocks we hold had varied returns: United Rentals was down 10.5%, Agricultural machinery producer Deere and Co. was down 9.8% (although steady from the start of the year). Residential house builder, DR Horton, fell 5% – this stock we think is very undervalued. We retain a very positive view of all these companies and valuations are quite attractive.

Interestingly, from an Australian investor’s perspective the fall in the global stocks, post tariffs imposition, was lessened by the 5% fall in the A$, so net/net the fall was reduced to about 5%, a much more palatable figure. This is not the way we would look at it – the decline in the A$ of 40% over the last 15 years is a severe indictment of government policy and economic performance.

Australian Equities

Peter Reed

Australian Equities Performance

Source: Bloomberg

The Australian equity market followed the lead of the US and other overseas markets to finish the March quarter 3.3% lower, resulting in an essentially flat (+2.2%) index return for the 12 months. Although the largest sector, financials, as well as industrials and utilities, were all strong over the period, this was not enough to offset sharp declines in the resource sectors, being energy and materials.

Notable during the quarter was the release of earnings for the period ended 31 December 2024. Against market expectations, results were broadly positive with approximately two companies outperforming expectations against one coming under.

More relevant to us were valuation issues in parts of the market, particularly among important sectors such as the banks. CBA was the major bank to report during the period, which has been the consistent outperformer among its peers. While the bank has arguably the best franchise in the sector – high market share, sound loan book and a customer base that has not been ceded to the mortgage brokers – the results were underwhelming, particularly against the valuation placed on the stock. The stock trades on a PE multiple of 25X and a price/book multiple of 3.3X. At these valuations, we would be looking for a significantly higher return than what the bank currently produces: 13.6% return on equity.

A feature during the reporting period was cases of extreme price volatility on the release of the results. A couple of portfolio holdings were subject to this:

Redox has been an outstanding performer in the portfolio since our acquisition shortly after its IPO. However, the company indicated a challenge in fully passing on commodity price rises, while higher operating costs further impacted margins. Against this, we view the company’s performance around volume and customer growth as solid and anticipate more attractive M&A opportunities to come. Ultimately, we remain positive on the business and believe the long-term growth opportunity remains unchanged.

Lindsay Transport was similarly impacted following the release of its results, with the company indicating pressure on operating costs, at the same time as trucking rates were squeezed by increased capacity coming into the industry. We would expect these price pressures to settle over time and see the prospect of a turnaround in rates as capacity is removed. We believe some businesses are operating at sub-economic rates and wouldn’t discount the possibility of another Scotts-type collapse. With Lindsay trading at a sub-10 price-earnings multiple, such a scenario would provide the basis for a re-rate of the stock.

Positively, results for our newly acquired property stock, Dexus, were solid, and give us confidence that the company is well positioned to benefit from exposure to the premium end of the office market. We expect demand conditions for this segment to remain positive and significantly better than the lower grades; the premiumisation trend has further to run whilst supply growth remains manageable.

Ventia, another newly acquired position, bounced strongly post its results. The stock price has been negatively impacted by news that the ACCC was investigating possible acts of collusion involving Ventia. This was in relation to the pricing of contracts to the Department of Defence, allegations the company denies.

Putting this case aside, the company delivered a solid set of results with strong revenue growth (+7.6%) and double-digit profit growth of 12.8%. The company also pointed to further growth in an already solid order book, supporting future growth.

A comment on building products company James Hardie: Although the company is dealing with weakness in segments of its market in the US, namely the multi-family segment, quarterly results announced during the period were ahead of market expectations and the company maintained its FY25 guidance.

What did surprise the market, however, was the announcement by Hardies of an acquisition of building products company Azek, which manufactures decking and railing outdoor products. With a total value of $8.75bil, this is a large acquisition. Based off a purchase multiple of 34X FY26 expected earnings, we would also draw the simple conclusion that it is expensive, in spite of indicated synergies, both cost and commercial, of $350m. This seems to fit a pattern of companies over-paying for acquisitions.

Although we question the company’s strategy, given the sharp pullback in share price, our view at this point is to maintain our holding and assess progress of the newly acquired business, particularly over targeted synergies. We see some prospect for price support from a listing of the company on the NY stock exchange, which if it does eventuate, may allow for further review of the position.

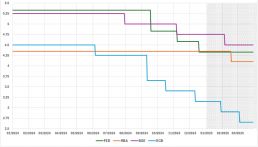

Finally, last quarter when we showed the valuation chart of the market it was close to the 1 standard deviation line, indicating overvaluation against its historical range. The pull-back in the market over the quarter has brought this level closer to average. With continued uncertainty over policy direction in the US, particularly over tariffs, prospects for further market weakness cannot be ruled out. This will potentially open further buying opportunities for the portfolios.

ASX200 Price to Earnings Ratio (P/E)

Source: Bloomberg

The sharp pullback in the equity market following the announcement of US tariffs will push this chart lower, most likely taking it under the long-term average. We note that given the US is not a major market for Australian exporters, first order impacts will likely not be as great as for some other countries. Rather, it’s the second order impacts which are likely to be more significant, such as for our miners with demand from major customers in China, Japan, Korea and elsewhere.

Interest Rates

Neil Sahai

90 Day Bank Bill (%) vs 10 Year Bond (%) Performance

Source: Bloomberg

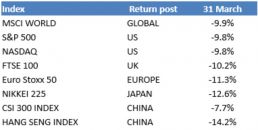

The first quarter of 2025 saw a cautious approach to monetary policy amid persistent but moderating inflation and global economic uncertainties. The Federal Reserve (Fed) maintained its interest rate range at 4.25%-4.5%, revising expectations for cuts due to strong employment data and lingering inflation. The Bank of England (BoE) cut rates by 25 bps to 4.5% in February, then held steady in March, signalling a measured approach. The European Central Bank (ECB) reduced its deposit facility rate to 2.5% with 25 bps cuts in January and again in March, reflecting softening economic conditions. The Reserve Bank of Australia (RBA) cut rates by 25 bps to 4.1% in February, citing easing inflation and slowing wage growth, then held in April, awaiting further data. Meanwhile, the Bank of Japan (BOJ) continued its tightening trajectory, supporting upward pressure on Japanese government bond yields.

Central Bank Policy Cash Rates

Source: BloombergNote: The FED rate is the mid-point of the upper and lower bound rates.

US 10-year bond yields fell slightly while UK and Australian 10-year yields steepened, reflecting a more normalised curve after a period of inversion. However, ongoing rate uncertainty may contribute to market volatility.

10 Year Bond Yields

Source: Bloomberg

The global interest rate outlook remains uncertain amid US tariffs, potential trade tensions, and moderating growth. However, central banks have not committed to any course of action. Most importantly, the US Federal Reserve has

expressed the view that the tariffs, in themselves, will not be the determinant factor in proximate policy decisions.

Property (REITS)

Franklin Djohan

ASX Property Graph

Source: Bloomberg

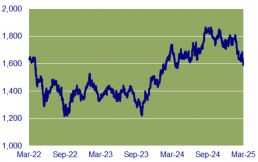

The A-REIT ASX 200 Accumulation Index declined by 6.8% for the quarter, effectively erasing all gains made so far in the financial year. While the property index underperformed the broader market, the decline was not broad-based.

The majority of the fall can be attributed to Goodman Group, which dropped 20.23% for the quarter. In February, Goodman announced a $4 billion equity raising to fund its data centre expansion plans. This came at a time when the broader market was experiencing volatility—particularly among AI-related stocks and data centre companies. Concerns around profitability and potential overinvestment in the sector contributed to the sell-off, with Goodman among the most affected. Similarly, DigiCo Infrastructure REIT, a newly listed property fund focused on data centre assets, declined 32.58%, amid concerns it may have overpaid for some of its acquisitions.

However, it is not all doom and gloom for the property sector. Mirvac signalled in its most recent results that a market turnaround may be underway. The company highlighted several drivers for earnings growth in FY26 and beyond, including a robust pipeline of development projects, a high-quality investment portfolio generating recurring income, and contributions from its established funds management platform. Mirvac appears well positioned to benefit from a sector recovery, supported by easing inflation and growing expectations that interest rates will decline. Its share price rose 11.47% over the quarter.

Charter Hall Group, a listed property fund manager, delivered a strong performance, with its share price rising 12.75% for the quarter. The company echoed Mirvac’s positive outlook and upgraded its FY25 earnings guidance.

Similarly, Ingenia Communities Group, which focuses on lifestyle communities, also reported strong results, and upgraded its FY25 earnings guidance, forecasting 20–23% growth from the previous financial year. Its share price rose 18.34% for the quarter.

PPM is continuously looking for ways to improve the service we provide to you and your feedback is important to us. We hope are staying safe and healthy. Please contact Jill May, Head of Client Relations with any questions, comments or suggested improvements at jm@ppmfunds.com or on (02) 8256 3712.

Private Portfolio Managers Pty Limited ACN 069 865 827, AFSL 241058 (PPM). The information provided in this document is intended for general use only and is taken from sources which are believed to be accurate. PPM accepts no liability of any kind to any person who relies on the information contained in this document. The information presented, and products and services described in this document do not take into account any individuals objectives, financial situation or needs. The information provided does not constitute investment advice. You should assess whether the information is appropriate for you and consider talking to a financial adviser before making any investment decision. Past performance is not necessarily indicative of future returns. © Copyright Private Portfolio Managers Pty Limited ABN 50 069 865 827, AFS Licence No. 241058.

Your Investment Management Team

Hugh MacNally

Portfolio Manager,

Executive Chairman

Peter Reed

Portfolio Manager,

Director

Franklin Djohan

Portfolio Manager / Analyst

Max Herron-Vellacott

Portfolio Manager

Neil Sahai

Portfolio Manager